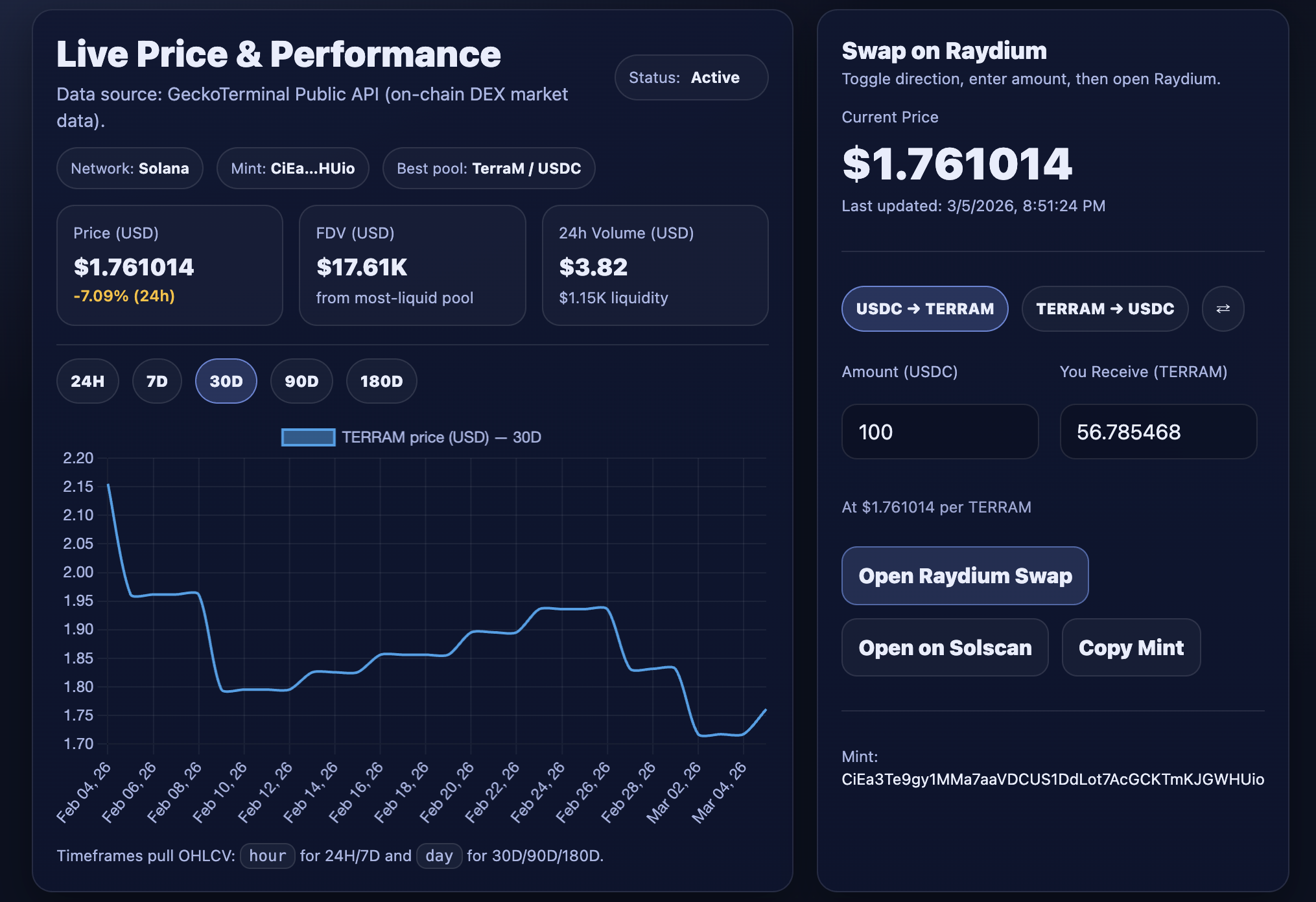

On March 6, 2026, the TerraM token traded at $1.76, down 10.65% week over week. On-chain activity was limited during the period, with two buys and one sell.

The sell order was large enough to push the price down significantly. The positive side is that it increased overall liquidity. With a few additional buybacks, the price could recover on a stronger liquidity base. That’s positive.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 3.25% of total supply.

Because of the selloff in the TerraM token, the fully diluted market capitalization decreased by approximately $2,100 week over week, settling at $17,600. The $20K level still appears within reach, and we remain confident it can be achieved by the end of the month, provided there is no significant selling pressure.

Our broader objective remains expanding liquidity coverage to 10%, and we’re pleased to have finally surpassed the 3% mark. The next short-term milestone is reaching 4%, which we expect to achieve by the end of the month, with continued buybacks in operation we also expect token price to stabilize around $2 by that time.

Until liquidity deepens further, elevated slippage should be expected.

Ethereum Strategy

Week over week, the Ethereum strategy expanded by 1.42%. We slightly lagged the broader market recovery, as part of our holdings were capped by covered calls that ended up in the money.

From the all-time high in September 2025, the fund is still down -70.77%. While YTD performance stands at -36.39%, underperforming ETH itself, which is down -30.52% over the same period.

During the week, the ETH Strategy generated $76 in options premiums, reducing the effective ETH break-even price to $1,702. By week’s end, the strategy held 2.025ETH with an average acquisition price of $1,982.

From the options premium received, we reduced margin debt to –$1,713. Our margin actually increased slightly week over week, but not because we borrowed more, but because we rolled an in-the-money covered call up and out, still for a credit. In the longer term, if we manage to close the position below our strike price (2050), the margin will decrease by roughly $180 to $1,533.

The immediate objective is to bring margin back to zero without selling any ETH. After that, depending on market conditions, we may increase exposure by adding 1 additional ETH on margin. Time will determine the right moment.

At an average premium of $76 per week, it would take approximately 22 weeks to eliminate the remaining margin balance — around start of August. We will maintain our current trading strategy throughout March but may add limited exposure to target at least $100 in weekly income.

Solana Strategy

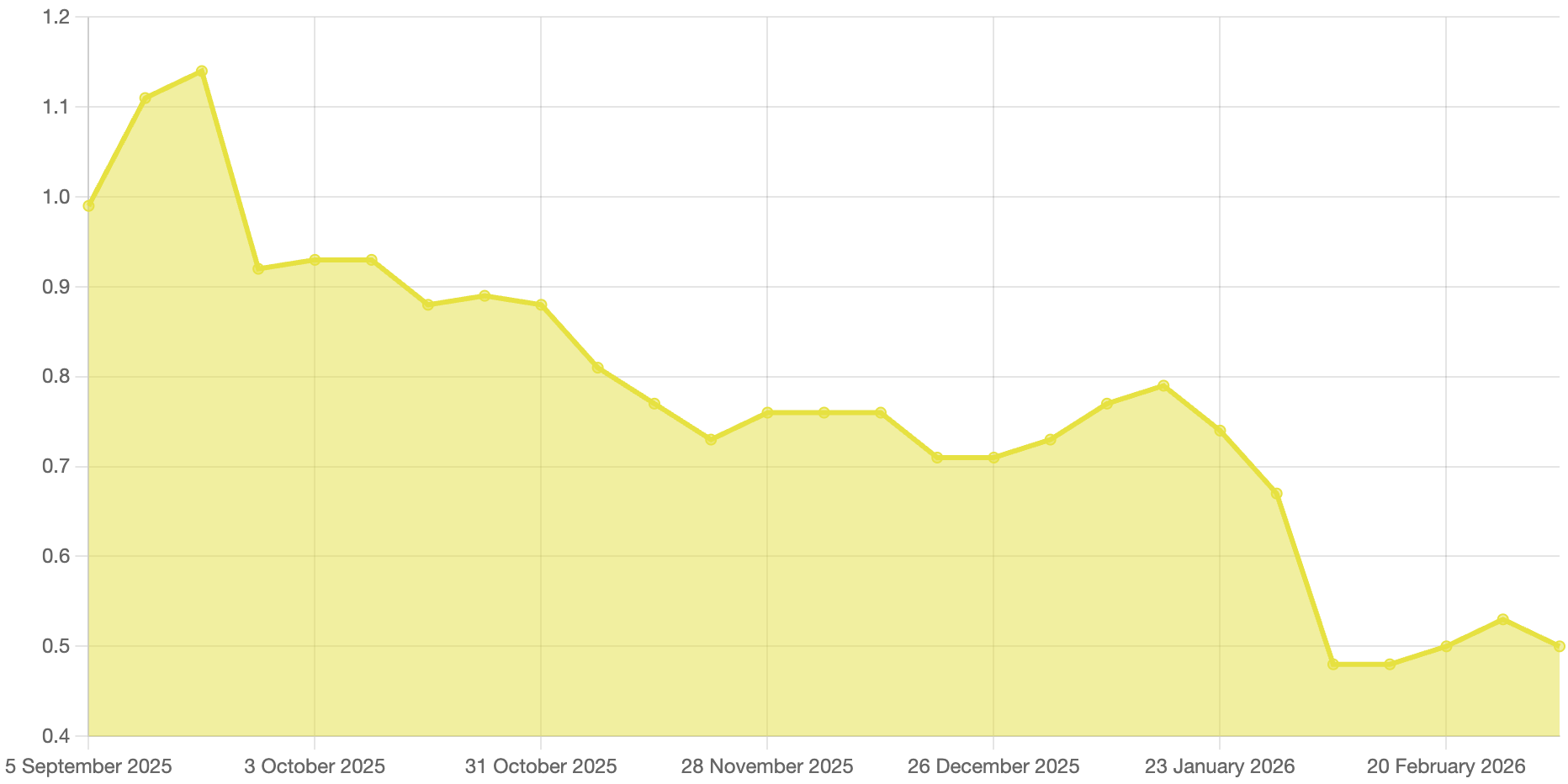

The Solana strategy decreased by -4.31% week over week, with NAV dropping to $0.50.

The drop is mostly technical rather than fundamental. SOL itself actually increased this week. The decline comes from converting part of the fund’s cash holdings into TerraM tokens; since TerraM fell about 10% this week, it affected the reported performance of the SOL fund.

Currently, the SOL Fund holds around 1,500 TerraM tokens. Earlier, we used cash reserves to help stabilize the main ETH fund during the February market stress, and these tokens temporarily replaced part of that cash balance.

A TerraM price of about 1.85 would neutralize the current loss. Since this is an internal allocation, we take full responsibility and stand ready to buy back these tokens at 1.85 at any time.

At the same time, we believe in the long-term value of the TerraM token. However, the intention is not to keep this exposure indefinitely — we plan to gradually exit the position within a reasonable timeframe through weekly or monthly buybacks, returning the SOL fund to a more standard asset composition.

By the end of the week, we increased our long spot position to 54.54 SOL, with a buy price at $163.60 and break-even price of $146.29. With Solana trading at $88.02 at the time of writing, the position is still significantly underwater.

During the week, we collected $22.33 in option premium by selling 9 weekly calls and 2 calls expiring on April 24, 2026.

Because the position is currently underwater, our flexibility is limited. To generate meaningful premium, we had to sell calls below our average entry price, effectively capping part of the upside recovery.

Overall our Solana Strategy YTD performance is -32.66%, just slightly underperforming SOL itself, which is down -29.29% over the same period. Solana is high risk / high reward investment

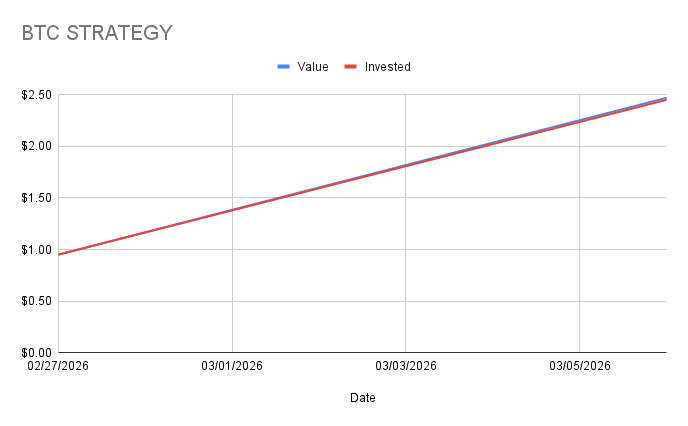

Bitcoin Strategy

This week we allocated 2% of total options income to buy spot BTC, increasing our holdings to 0.00003506 BTC.

After the first week, our Bitcoin strategy is up 0.47%, which is a good start.

Market Outlook

BTC is currently trading below its 50- and 200-day moving averages and is testing resistance around $76,000. A clear break above this level would be the first meaningful signal of potential bullish continuation. If that resistance is overcome, the next key level appears near $89,000, which would complete the so-called cup pattern.

Another point worth noting is the BTC/ETH ratio, currently around 0.0292. If Bitcoin were to reach $89,000 while the ratio remains roughly stable, that would imply an ETH price near $2,600.

Food for thought — not a trade recommendation.

The bottom line

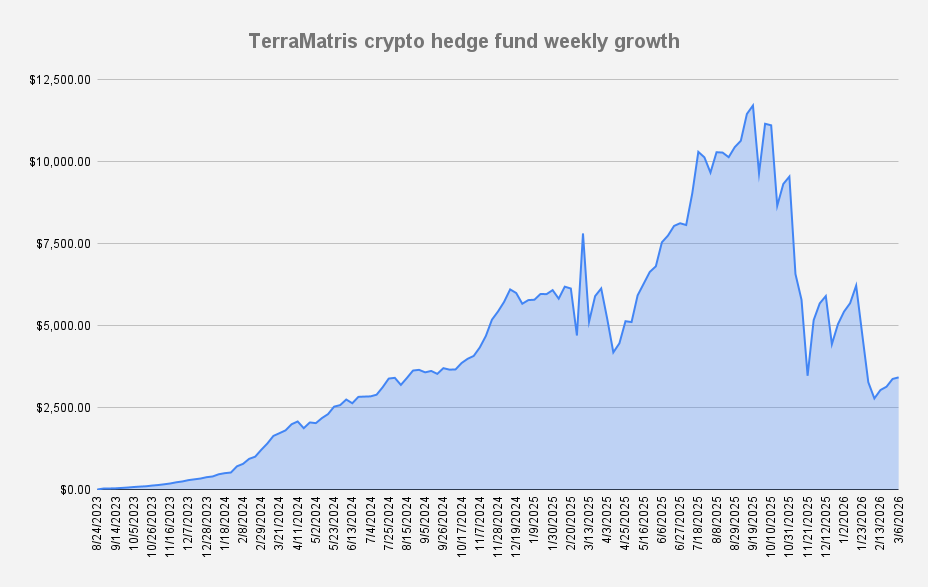

TerraM token experienced a volatile week mainly due to limited liquidity and a single larger sell order, but the situation also improved the market structure by increasing available liquidity.

- The Ethereum strategy continues its slow recovery phase. Options premiums are steadily reducing margin exposure while preserving the core ETH position.

- The Solana strategy remains significantly underwater due to the broader SOL drawdown, though the position continues generating option income.

- The Bitcoin strategy is still in its early accumulation phase. While the position is small, it is already slightly positive and will continue to grow through systematic purchases funded by options income.

Overall, the focus across the fund remains on stabilization, disciplined income generation, and improving liquidity. Despite the difficult market environment, the strategies continue operating as intended—collecting premiums, strengthening internal liquidity, and positioning the portfolio for the next market recovery cycle.