As of July 10, 2026, our Ethereum strategy portfolio was valued at $3,205, up 5.4% week over week. Despite the weekly recovery, the portfolio remains down -40.48% year to date and -72.65% below the all-time high reached in September 2025.

Based on our performance tracking, the strategy is slightly underperforming Ethereum itself, which is down approximately 40.30% year to date.

Ethereum Covered Call Position

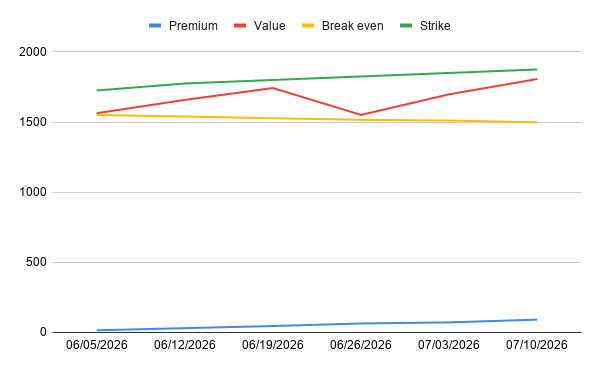

On July 7, just a few days before expiry, we decided to roll our 1.3 ETH covered call position up and forward.

We bought back the $1,850 call for $13.40 and sold the July 17 $1,875 call for $29.60. Based on the quoted option prices, the roll generated a gross credit of approximately $16.20 before fees.

According to our portfolio calculations, this increased the total potential profit from the position to $523.15 over 42 days. If ETH trades above $1,875 and the position is called away at expiry, the trade would generate a potential return of approximately 25.37% over that period.

This return includes both the options premiums collected and the potential capital gain on the underlying ETH position. It is therefore a return on the complete covered call trade rather than options income alone.

If the position is closed at $1,875, we plan to allocate half of the realized gains to TerraM token treasury operations.

TerraM Token

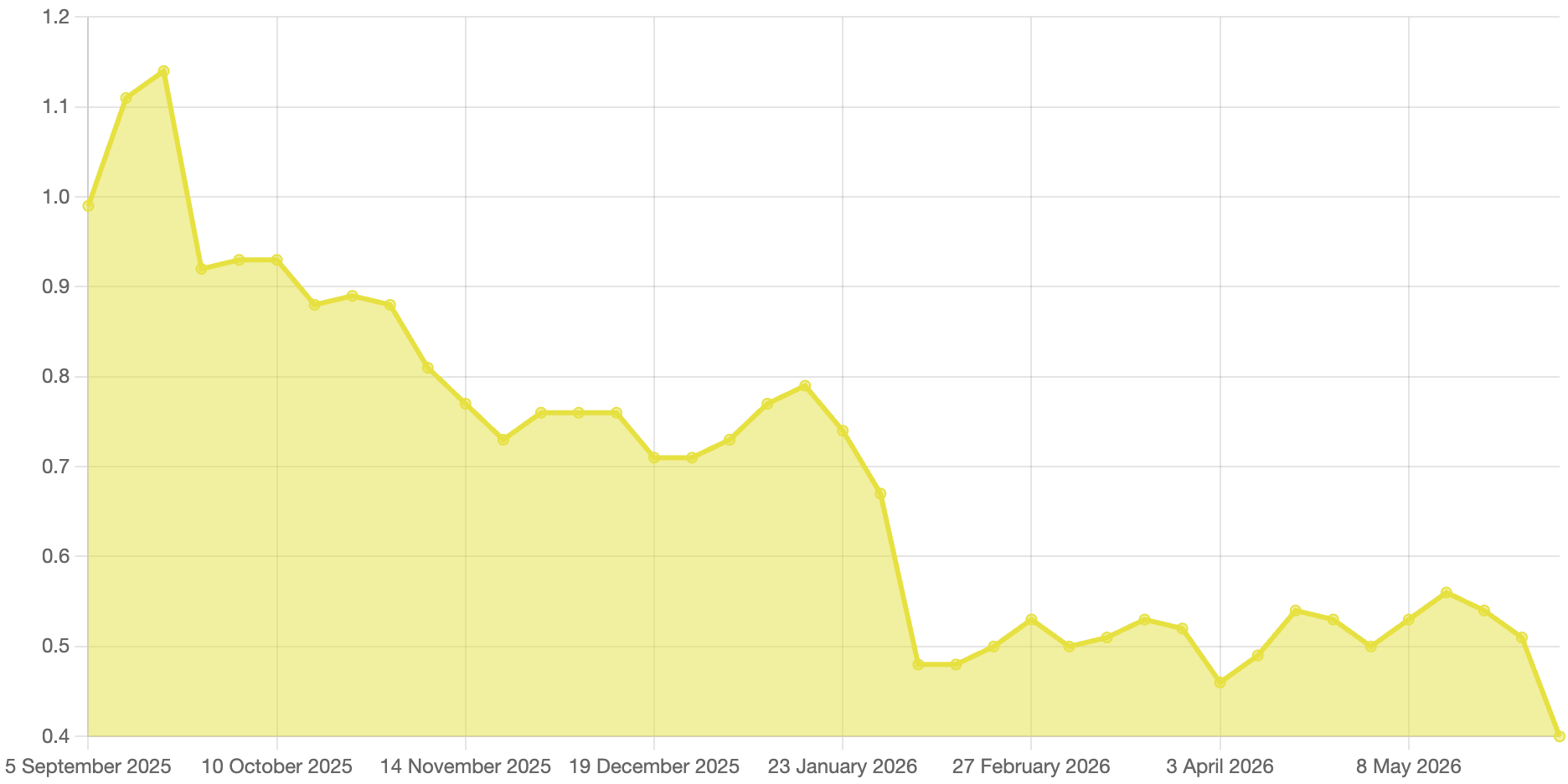

Speaking of TerraM, it was an unusually volatile week. At one point, the TerraM token traded at an all-time high of $6.26 before falling back to approximately $0.54. The move represented an increase of more than tenfold, but the majority of the rally lasted only a few hours.

One of our treasury goals is to maintain liquidity equal to at least 10% of the TerraM token value in the Raydium liquidity pool. Liquidity is currently above that target.

A future treasury buyback would place additional buying pressure on the pool and could increase the token price by several percentage points, depending on the size of the transaction and the available liquidity. However, this should not be treated as a guaranteed or lasting price increase, particularly given TerraM's limited liquidity and the extreme volatility seen during the week.

Solana Covered Call Fund

The Solana strategy decreased by 0.55% week over week. NAV per unit remained approximately flat at $0.33, with the difference largely explained by rounding.

By the end of the week, our long spot position stood at 85.16 SOL, with an average purchase price of $151.81 and a break-even price of approximately $132.70. With Solana trading near $78 at the time of writing, the position remains significantly underwater.

During the week, we collected $12.80 in options premium by selling covered calls expiring at the end of July and August. Only a small portion of the SOL position was covered, leaving most of our spot holdings uncapped to preserve upside potential in the event of a broader market rebound.

The Solana strategy is down 55.74% year to date, compared with a decline of approximately 36.68% for SOL itself. The underperformance reflects not only the decline in SOL but also losses associated with the TerraM allocation and the limited options income generated while the underlying position remained far below its break-even price.

Bottom Line

The Ethereum strategy showed a meaningful weekly recovery, but both the ETH and SOL portfolios remain deeply below their previous highs. The decision to roll the ETH covered call up to $1,875 increased the potential exit price while still generating additional premium.

On the Solana side, we are taking a cautious approach. Selling calls against only a small portion of the holdings produces some income without placing a hard ceiling on most of the position if SOL rebounds.

TerraM's brief tenfold move demonstrated how quickly a small and relatively illiquid token can rise, but also how quickly those gains can disappear. Our priority remains improving liquidity, managing treasury capital conservatively and avoiding decisions based on temporary price spikes.

Overall, the portfolios remain in recovery mode. Options premiums are helping to reduce the effective break-even prices, but the main driver of future performance will still be a sustained recovery in ETH and SOL rather than premium income alone.