Research

Backtesting Ethereum: How Often Does ETH Drop 5% in a Day?

While working with the TerraM trading bot, I conducted a backtest to quantify the frequency of significant daily drawdowns over the past 365 days (May 4, 2025 – May 3, 2026). Specifically, I analyzed how often the daily price change exceeded -5% or more. The results are notable.

The dataset is based on historical price data sourced from CoinMarketCap, with calculations performed in Google Sheets. Daily performance was measured as the percentage change between the open and close prices.

Out of 365 trading days—reflecting the continuous nature of crypto markets—194 days closed…

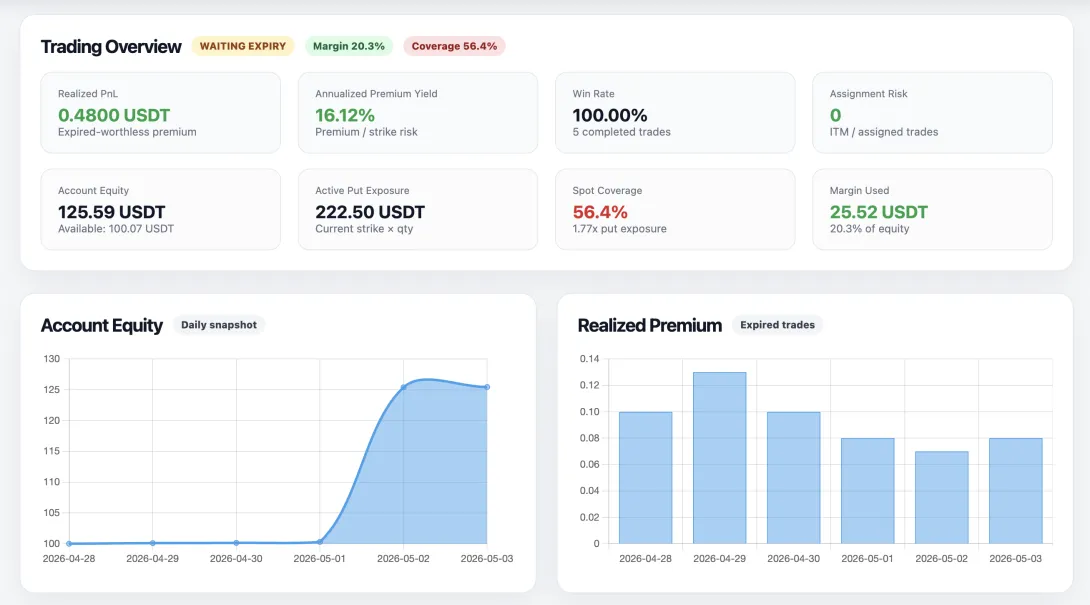

Discovering Derive: Our First Steps into True DEX Options Trading

At Terramatris, we’ve always been fascinated by the evolution of crypto markets and the growing range of opportunities they create for traders and investors. For years, our main focus has been on more traditional centralized exchanges (CEX) such as Bybit and Deribit. These platforms have provided liquidity, stability, and advanced trading features—making them indispensable for our operations.

But one thing has always been missing: a true decentralized exchange (DEX) for options trading.

Recently, while researching potential institutional partners for our US operations (Kraken…

Why We Decided to Invest in Liberland Dollar (LLD)

At Terramatris, we are always exploring opportunities that align with our values of innovation, independence, and forward-thinking. Sometimes, these discoveries come through structured research, and sometimes they appear unexpectedly. Our recent investment into Liberland Dollar (LLD) belongs to the second category — a pleasant surprise during our ongoing research into projects that combine crypto innovation with strong community values.

Over the past year, we’ve attended few crypto-related meetups and brunches in Tbilisi, Georgia, a city that has become a lively hub for blockchain…

Wishful Thinking, Statistics, and Modeling: Where Could Terramatris Fund Be in September 2026?

On September 2, 2025, the Terramatris crypto hedge fund stands at $10,500. Out of this, roughly $3,500 is low-interest debt, which we are steadily repaying at a rate of $300–450 per month. If nothing changes, we expect to be debt-free by April 2026. Importantly, there is no real pressure to return these funds quickly; and if market conditions turn against us, we believe we could borrow back on similar terms without risk to the core strategy.

This puts Terramatris in a comfortable position: a five-figure portfolio, a clear debt-repayment path, and a robust options premium strategy…

Snipping in DeFi: Tempting, But Not Sustainable

At Terramatris, we constantly evaluate emerging strategies in the decentralized finance (DeFi) landscape — especially those that promise asymmetric upside. One such tactic is snipping (or sniping), a method that’s gained attention for its high-speed, high-risk approach to token trading.

We want to offer a clear and honest take: while snipping can be entertaining and, in rare cases, wildly profitable, it doesn’t align with our long-term trading philosophy.

What Is Snipping in DeFi?Snipping refers to the practice of purchasing newly launched tokens at the exact moment liquidity…