At the beginning of June, we reached a turning point.

Once again, we experienced a scenario that has hurt our portfolio several times over the years. We were holding profitable long positions while simultaneously opening additional short positions using borrowed funds. The idea was to hedge risk and generate returns from both sides of the market.

Instead, the market moved sharply against us.

As Ethereum fell toward $1,500, tail risk increased dramatically. Our long positions lost value, while our short positions also became problematic due to the structure and leverage involved. Rather than reducing risk, the strategy created complexity, stress, and capital inefficiency.

At that point, we concluded that continuing to fight this battle was no longer worthwhile. Some investors may disagree with this decision, but after several years of experimentation, we believe a simpler approach offers a better risk-adjusted return profile.

As a result, we have decided to transition away from active long/short trading and focus primarily on a strategy we know well: owning Ethereum and generating income through covered call writing.

Our goal is not to maximize upside. Instead, we aim to generate consistent cash flow by selling out-of-the-money covered calls, typically around a 0.15 delta, while maintaining long-term exposure to Ethereum.

Investors interested in learning more about this approach can review our educational guides:

The TerraM Token

This strategic transition also required us to withdraw capital from several areas of the portfolio. Unfortunately, that included selling a significant number of TerraM tokens.

The positive news is that we have increased liquidity in the Raydium liquidity pool to over 10%, with the current liquidity ratio standing at 10.35%, which is a healthy level.

The downside is that the token price has declined to approximately $0.54 per token. The good news is that the price could be lifted relatively quickly with additional buying activity on Raydium.

If you would like to participate, we encourage purchases through the Raydium liquidity pool, as this directly supports market depth and price stability. Otherwise, it may take some time before we can restore the token price to its previous range of $2–$3 per token.

For nearly four years, the TerraM token has been an experiment. While it has served its purpose and helped us build a community around the fund, it never achieved the scale or utility we originally envisioned.

We are not abandoning TerraM.

We will continue honoring all existing commitments and obligations related to the token. Nothing changes for current holders in that regard. However, we no longer believe it makes sense to structure the entire fund around a token whose primary function is to sit in a liquidity pool while productive capital opportunities exist elsewhere.

Going forward, Terramatris will focus less on the token itself and more on what has been our core activity for almost three years: generating returns through Ethereum options strategies.

There have been successes and setbacks along the way, but covered call writing remains the strategy we understand best and the one we believe offers the most attractive balance between risk and reward.

Going forward, we will no longer distribute option income to the fund on a weekly basis. Instead, 50% of the realized option income will be allocated only after a position has been closed and profits have been secured.

This approach allows us to retain more working capital during the life of a trade while ensuring that distributions are based on realized, rather than anticipated, returns.

Ethereum strategy - First Trade Under the New Approach

On June 5, 2026, we purchased 1.3 ETH at $1,563 and simultaneously sold covered call options expiring on June 12, 2026, with a strike price of $1,725. The trade generated option premium income of approximately $12.30 per ETH.

One week later, on June 12, the options expired worthless, allowing us to keep the full premium while retaining ownership of the ETH. We then immediately sold another covered call with a June 19, 2026 expiration date.

The strategy is straightforward.

If ETH trades above the strike price at expiration, we realize our maximum profit and the position is called away. If ETH remains below the strike price, the options expire worthless, we keep the premium, and we can sell another covered call for the following week.

One of the most important aspects of covered call writing is strike price selection. The strike determines both the premium received and the potential upside retained in the underlying asset.

To learn more about our methodology, see: How to Choose Strike Prices for Ethereum Covered Calls.

Trade Metrics

- ETH Purchase Price: $1,563

- Strike Price: $1,775

- Premium Collected: $23.81 per ETH

- Maximum Profit: Approximately $307.45

- Holding Period: 13 Days

- Break-even Price: $1,539

The maximum profit represents roughly an 15.08% return over 13 days. While this annualizes to an extraordinary percentage, such figures should not be interpreted as sustainable long-term returns. They simply reflect the unusually high option premiums available during periods of elevated volatility.

What Happens Next?

Scenario 1: ETH Remains Below $1,775

If ETH stays below the strike price at expiration, the options expire worthless.

We retain the premium, continue holding the ETH position, and can generate additional income by selling another covered call.

Scenario 2: ETH Rises Above $1,775

If ETH closes at or above the strike price, the position achieves its maximum profit.

The ETH is called away, capital is released, and we can either establish a new covered call position or pursue another opportunity.

In both scenarios, the outcome is clearly defined from the moment the trade is entered. The only variable is where Ethereum is trading at expiration.

If this position reaches its maximum profit target, we plan to allocate 50% of the realized profit back to the TerraM token liquidity pool on Raydium. The remaining capital will be recycled into new income-generating positions.

Our preferred next step would be to re-enter the market by selling cash-secured put options. Depending on market conditions and available premiums, we may also consider deploying defined-risk strategies such as credit spreads to enhance capital efficiency while maintaining controlled risk exposure.

Solana Strategy

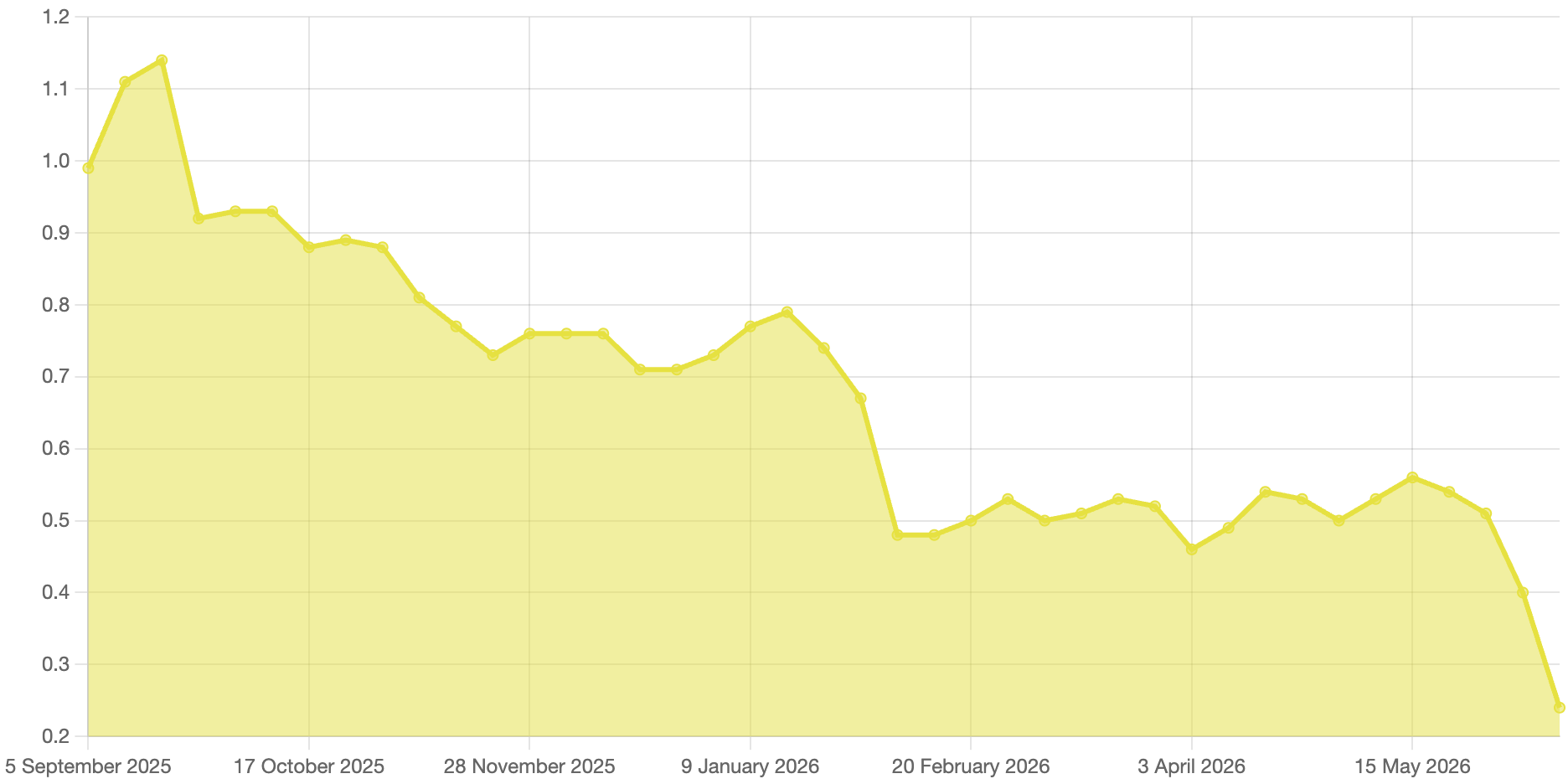

Solana strategy was not saved either and decreased by another -40.50%. NAV per unit decreased to $0.24, while SOL was trading at approximately $67 per token.

It should be noted that this decline is primarily attributable to the SOL Fund's holding of approximately 1,200 TerraM tokens. The decrease in value is therefore largely driven by the depreciation of the TerraM token itself rather than by the performance of Solana or the underlying SOL position.

By the end of the week, we increased our long spot position to 73.07 SOL, with a buy price at $162.40 and break-even price of $140.55. With Solana trading at $67 at the time of writing, the position is significantly underwater.

Solana Strategy YTD performance is -68.00%, slightly outperforming SOL itself, which is down 46.02% over the same period.

What's Next?

June marks the beginning of a new chapter for Terramatris.

After several years of experimenting with increasingly complex long/short strategies, leverage, perpetual futures, and multi-layer portfolio structures, we have decided to simplify our approach and focus on what has consistently worked best for us: generating income through Ethereum options.

Our primary objective for the remainder of 2026 is straightforward: accumulate Ethereum, generate recurring option premium income, preserve capital, and allow profits to compound over time.

Rather than attempting to predict short-term market direction, we intend to focus on repeatable processes. Covered call writing allows us to generate income whether the market moves sideways, rises modestly, or even experiences periods of elevated volatility.

If our current Ethereum covered call position reaches maximum profit, we intend to allocate 50% of realized profits back to the TerraM liquidity pool on Raydium. The remaining capital will be redeployed into new income-generating positions.

Our preferred next step after a successful covered call cycle is to sell cash-secured put options. This strategy allows us to continue collecting option premium while potentially acquiring additional ETH at attractive prices.

Depending on market conditions, we may also selectively deploy defined-risk strategies such as credit spreads when they offer favorable risk-adjusted returns. However, unlike previous years, these positions will remain secondary to our core covered call strategy.

TerraM Token Outlook

TerraM remains an important part of the Terramatris ecosystem, but its role is evolving.

Our immediate focus is improving liquidity and strengthening the market structure around the token. We believe healthy liquidity is more important than short-term price movements and provides a stronger foundation for future growth.

Future support for the liquidity pool will come primarily from realized trading profits rather than borrowed capital or speculative interventions.

Solana Portfolio Outlook

The Solana portfolio remains significantly affected by the decline in both SOL and TerraM valuations. While current performance is disappointing, we continue to hold the underlying SOL position and maintain exposure to any future recovery in the asset.

Our focus is no longer on maximizing growth through aggressive positioning but rather on capital preservation, portfolio efficiency, and disciplined risk management.

Final Thoughts

The decisions outlined in this report were not made because of a single losing trade or a temporary market decline. They are the result of several years of experience, experimentation, and observation.

Complexity often creates the illusion of better risk management. In practice, it can introduce additional risks that only become visible during periods of market stress.

Covered call writing is not a perfect strategy. It limits upside potential and does not eliminate downside risk. What it does provide is clarity, consistency, and a clearly defined framework for generating income.

As we move into the second half of 2026, our focus is simple: own quality assets, generate recurring option income, manage risk conservatively, and allow compounding to do the heavy lifting.

We believe this approach offers the best opportunity to rebuild net asset value while creating a more sustainable foundation for Terramatris in the years ahead.

Risk Disclosure

Past performance does not guarantee future results. Cryptocurrency investing and options trading involve substantial risk, including the possible loss of principal. This report is provided for informational and educational purposes only and should not be considered investment advice. Investors should conduct their own research and consult qualified financial professionals before making investment decisions.