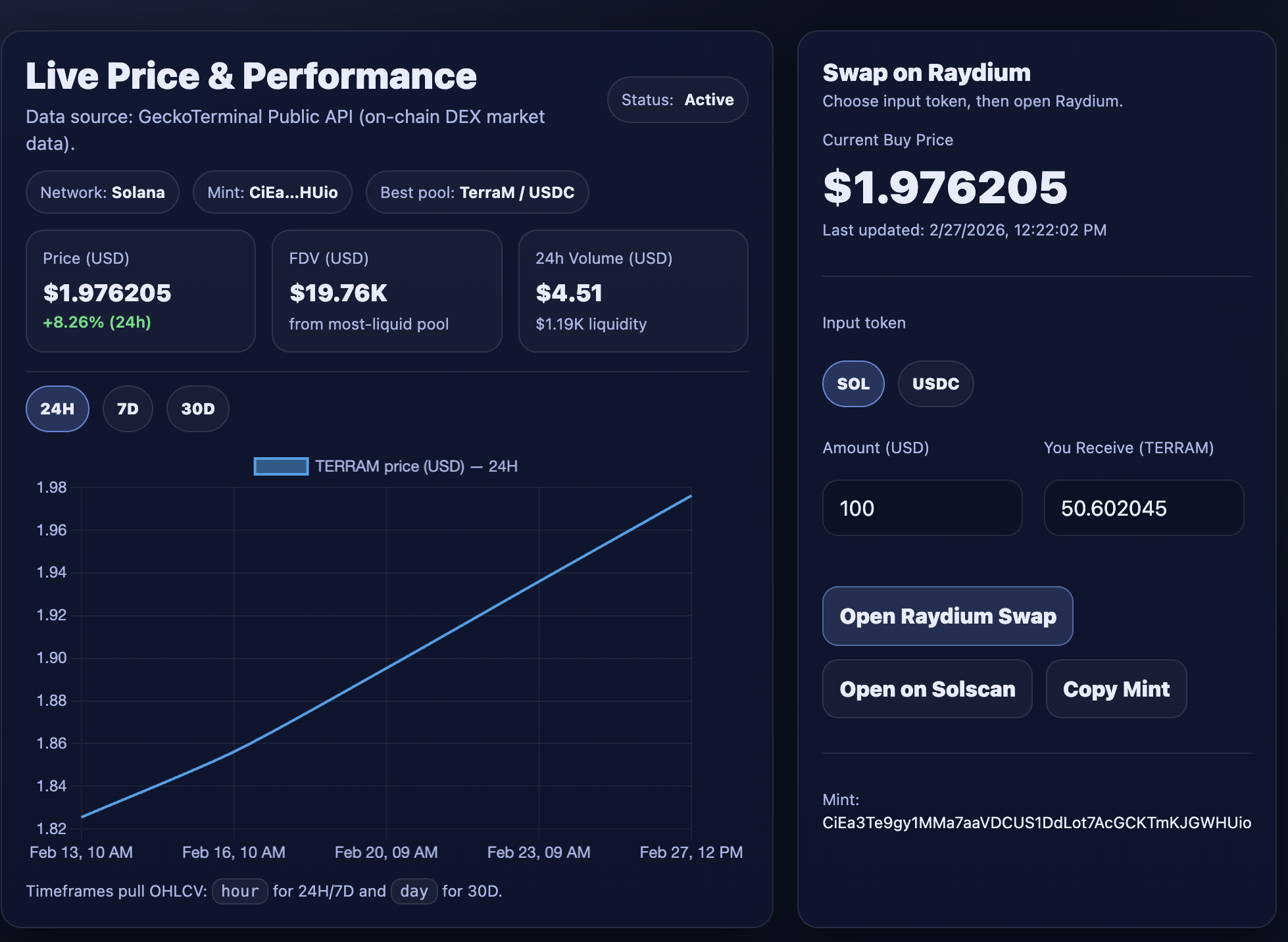

On February 27, 2026, the TerraM token traded at $1.97, up 4.23% week over week. On-chain activity was limited during the period, with two buys and no sells. For a nano crypto fund like ours, every on-chain transaction is an event worth noting.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 2.98% of total supply. As a result, total market capitalization, if fully distributed, increased by approximately $800, reaching $19,700 week over week. $20K feels within reach. Let’s aim to break above that level next week.

That said, these figures are still useful as a reference point — without meaningful liquidity, slippage becomes excessive.

Our broader objective remains expanding liquidity coverage to 10%, with the next milestone set at 3%. We expected to reach this minor milestone already this week. However, two buybacks removed roughly 0.06% of liquidity from the pool, slightly delaying the move. We remain confident that the milestone will be reached next week.

Until liquidity deepens further, elevated slippage should be expected.

Ethereum Strategy

Week over week, the Ethereum strategy expanded by 7.56%. Solid result.

From the all-time high in September 2025, the fund is still down -71.18%. While YTD performance stands at -37.28%, underperforming ETH itself, which is down -31.39% over the same period.

During the week, the ETH Strategy generated $90 in options premiums, reducing the effective ETH break-even price to $1,740. By week’s end, the strategy held 2.025ETH with an average acquisition price of $1,982.

From the options premium received, we reduced margin to –$1,652. The immediate objective is to bring margin back to zero without selling any ETH. After that, depending on market conditions, we may increase exposure by adding 1 additional ETH on margin. Time will determine the right moment.

At an average premium of $90 per week, it would take approximately 18 weeks to eliminate the remaining margin balance — around start of July.

Solana Strategy

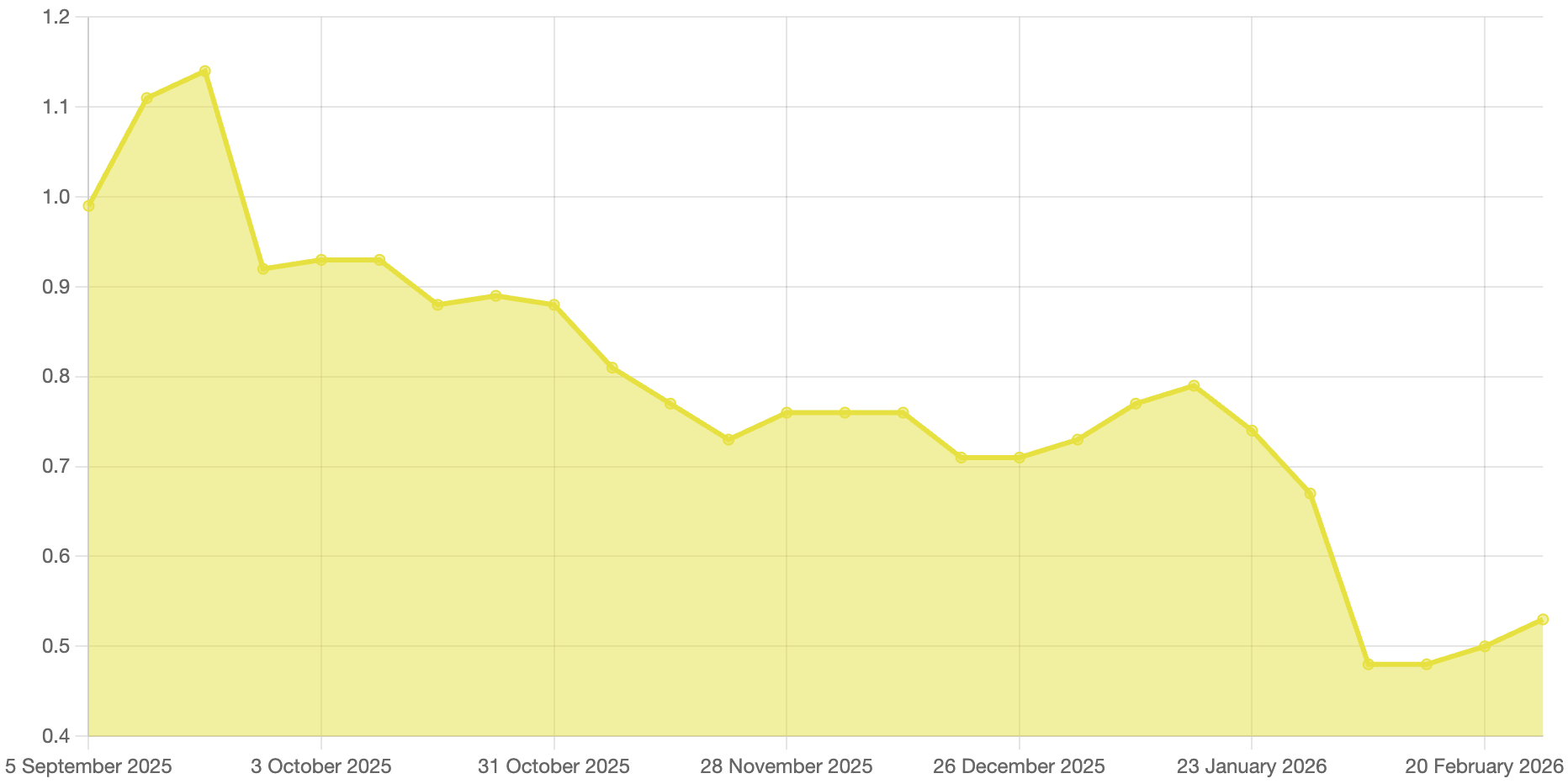

The Solana strategy increased by decent 5.05% week over week, with NAV reaching $0.53.

By the end of the week, we increased our long spot position to 54.29 SOL, with a buy price at $163.87 and break-even price of $146.81. With Solana trading at $87.27 at the time of writing, the position is still significantly underwater.

During the week, we collected $139.46 in option premium by rolling our existing Solana positions to the March 27 expiry.

Because the position is currently underwater, our flexibility is limited. To generate meaningful premium, we had to sell calls below our average entry price, effectively capping part of the upside recovery.

To balance premium collection with some retained upside exposure, we structured a 102/120 vertical call spread instead of selling a covered call. This allows us to collect income while still participating in price appreciation if there is strong rally above $120, rather than fully capping gains at the lower strike.

Overall our Solana Strategy YTD performance is -29.62%, just slightly outperforming SOL itself, which is down -29.84% over the same period. Solana is high risk / high reward investment

Bitcoin strategy

Starting today, we’re launching our Bitcoin strategy. For now, it’s spot-only.

We will reallocate 1% of the weekly options premium from the Ethereum strategy into spot BTC purchases, increasing the allocation by an additional 1% each week for 52 weeks (minimum $1 per transaction).

It will take time to grow into something meaningful, but to keep the framework simple and disciplined, we’re building it strictly as a spot strategy.

The bottom line

This was a decent week. Token price advanced, liquidity coverage moved closer to the 3% milestone, and both active strategies delivered positive week-over-week growth while continuing to generate steady option income.

Drawdowns remain significant, and margin is still a constraint, but risk is being managed deliberately: premiums are lowering break-evens, leverage is being reduced methodically, and exposure adjustments remain controlled.

The priority stays the same — strengthen liquidity, eliminate margin, and compound systematically. If execution remains consistent, gradual stabilization should precede recovery.