Blog

Ep 137: TerraM Eyes $2 as Liquidity Builds and Buybacks Continue

| Weekly updates | 12 seen

On April 3, 2026, the TerraM token traded at $1.85, down -8.4% week over week. On-chain activity was limited during the period, with two buys and one sell. The sell order pushed the price down but also increased pool liquidity; with a small buyback, we were able to stabilize the token.

During the week total TerraM liquidity on the Raydium pool increased to 3.63% of total supply.

Our broader objective remains to expand liquidity coverage to 10%, with a near-term milestone of reaching 4%. With continued buybacks in place, we expect TerraM to reach the $2–$2.2 range by the end of month, though some volatility should be expected.

Until liquidity deepens further, elevated slippage should be expected.

Ethereum strategyWeek over week, the Ethereum strategy…

Ep 136: TerraM Token Breaks $2 Again as Fund Continues Recovery Phase

| Weekly updates | 91 seen

On March 27, 2026, the TerraM token traded at $2.02, up 5.2% week over week. On-chain activity was limited during the period, with two buys and no sells. We’re genuinely excited to see the token break $2 again, though we expect continued volatility ahead.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 3.35% of total supply. As a result, total market capitalization increased by approximately $1,000, reaching $20,240.

Our broader objective remains to expand liquidity coverage to 10%, with a near-term milestone of reaching 4%. While we initially expected to hit this target by the end of this month, it now appears it may take another month. With continued buybacks in place, we expect TerraM…

Ep 135: TerraM Token Hits $1.92 (+4.94% WoW): Liquidity Expansion Targets $2 Breakout

| Weekly updates | 88 seen

On March 20, 2026, the TerraM token traded at $1.92, up 4.94% week over week. On-chain activity was limited during the period, with two buys and no sells. We expect trading activity to pick up once the token price moves above $2 and on-chain liquidity improves. This should particularly drive automated trading, with bots continuously scanning liquidity pools and exploiting arbitrage opportunities.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 3.3% of total supply.

Our broader objective remains expanding liquidity coverage to 10%, while the next short-term milestone is reaching 4%, which we expect to achieve by the end of the month, with continued buybacks in operation we also expect…

Ep 134: Ethereum Options Strategy Generates $112 as Crypto Market Recovers

| Weekly updates | 155 seen

On March 13, 2026, the TerraM token traded at $1.83, up 3.97% week over week. On-chain activity was limited during the period, with two buys and no sells.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 3.29% of total supply.

Our broader objective remains expanding liquidity coverage to 10%, while the next short-term milestone is reaching 4%, which we expect to achieve by the end of the month, with continued buybacks in operation we also expect token price to stabilize around $2 by that time.

Until liquidity deepens further, elevated slippage should be expected.

Ethereum strategyWeek over week, the Ethereum strategy gained 3.54%. During the week we ran a few…

Ep 133: TerraM Liquidity Expands After Selloff — Can the Token Return to $2?

| Weekly updates | 118 seen

On March 6, 2026, the TerraM token traded at $1.76, down 10.65% week over week. On-chain activity was limited during the period, with two buys and one sell.

The sell order was large enough to push the price down significantly. The positive side is that it increased overall liquidity. With a few additional buybacks, the price could recover on a stronger liquidity base. That’s positive.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 3.25% of total supply.

Because of the selloff in the TerraM token, the fully diluted market capitalization decreased by approximately $2,100 week over week, settling at $17,600. The $20K level still appears within reach, and we remain confident…

Ep 132: TerraM token at $1.97, Liquidity Expands, Market Cap Nears $20K

| Weekly updates | 165 seen

On February 27, 2026, the TerraM token traded at $1.97, up 4.23% week over week. On-chain activity was limited during the period, with two buys and no sells. For a nano crypto fund like ours, every on-chain transaction is an event worth noting.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 2.98% of total supply. As a result, total market capitalization, if fully distributed, increased by approximately $800, reaching $19,700 week over week. $20K feels within reach. Let’s aim to break above that level next week.

That said, these figures are still useful as a reference point — without meaningful liquidity, slippage becomes excessive.

Our broader objective remains expanding…

Ep 131: TerraM Liquidity Nears 3% Milestone as ETH Options Generate $99 Premium

| Weekly updates | 178 seen

On February 20, 2026, the TerraM token traded at $1.89, up 3.84% week over week. On-chain activity was limited during the period, with two buys and no sells, which is a positive signal.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 2.95% of total supply. As a result, total market capitalization increased by approximately $700, reaching $18,900 week over week.

Our broader objective remains expanding liquidity coverage to 10%, with the next milestone set at 3%. We expected to reach this minor milestone already this week. However, two buybacks removed roughly 0.05% of liquidity from the pool, slightly delaying the move. We remain confident that the milestone will be reached next week.

…Ep 130: TerraM Token Rises 2.8% as ETH Strategy Gains 9%

| Weekly updates | 200 seen

On February 13, 2026, the TerraM token traded at $1.82, up 2.82% week over week. On-chain activity was limited during the period, with two buys and no sells, which is a positive signal.

During the week, we added additional TerraM liquidity to the Raydium pool, increasing the share of fully USDC-backed TerraM tokens to 2.90% of total supply. As a result, total market capitalization increased by approximately $500, reaching $18,200 week over week.

Our broader objective remains expanding liquidity coverage to 10%, with the next milestone set at 3%. We expect to cross this threshold next week. Until liquidity deepens further, slippage is expected to remain elevated.

Ethereum StrategyOur first week as ETH only fund was decent, with fund value growing +9.21 week over week.…

Ep 129: Capitulation, Reset, and a Return to Spot-First Discipline

| Weekly updates | 268 seen

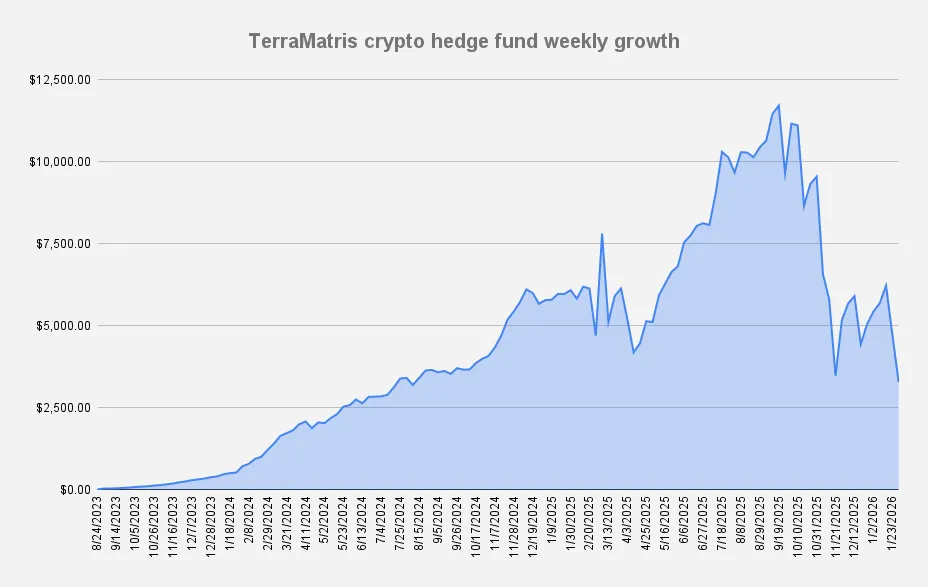

This week marked one of the most difficult moments in Terramatris’ history. The crypto market experienced a sharp and disorderly sell-off, and our portfolio entered what can only be described as a leverage-driven death spiral. At the peak of exposure, we were effectively controlling roughly 6 ETH with an average entry price above $3,500. Most of this exposure was expressed through perpetual futures and short put options, both of which moved deeply underwater as ETH collapsed. When Ethereum dipped below $2,000, the math stopped working.

At that point, we made a hard but necessary decision: unwind, realize losses, and move forward. We do not know whether this is the market bottom, nor whether a sharp recovery could follow quickly. What we do know is that continuing to operate under…

Ep 128: TerraM Token Rises to $2.83 (+2.9%) Despite Massive Crypto Selloff

| Weekly updates | 145 seen

On January 30, 2026, the TerraM token traded at $2.83, up 2.9% week over week. Trading activity increased following the launch of a 1 TerraM token weekly reward for liquidity staking. Automated trading bots quickly identified the incentive and began purchasing and staking TerraM tokens.

For most of the week, TerraM traded tightly around $2.90, before slipping to $2.83 on Friday morning amid short-term profit-taking by trading bots.

This bot trading development is positive. We estimate that 70–90% of DeFi activity is bot-driven, and as long as these bots are deploying real capital, their participation improves liquidity and market efficiency.

Bots, Rewards, and TerraM: Unexpected Signals from DeFi Liquidity

Looking ahead, we plan to continue using staking rewards…